{kind=link}

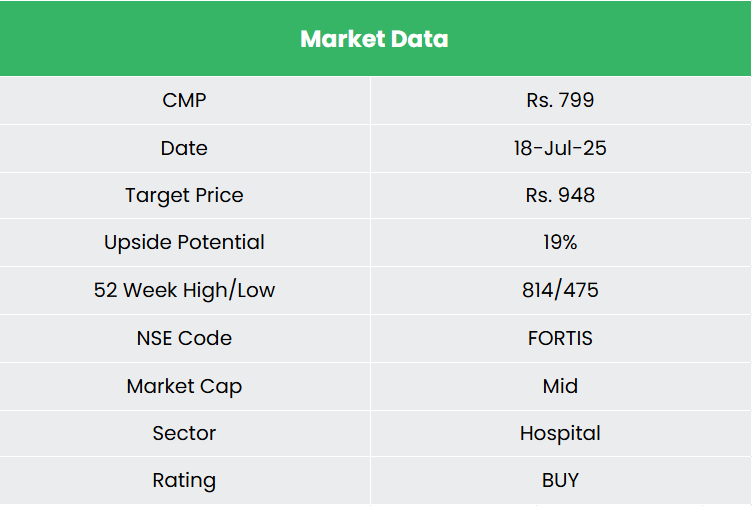

Fortis Healthcare Ltd – Transforming lives, Growing Together

Incorporated in 1996 and headquartered in Gurugram, Fortis Healthcare Ltd. is one of the largest healthcare services providers in India. The company provides a wide spectrum of integrated healthcare facilities comprising of hospitals, diagnostics and day care specialty hospitals. As of 31 March 2025, the company has a network of 27 hospitals across 10 cities, 7,500+ doctors, 7,500+ nurses, ~4,750 operational beds. Additionally, the company operates its network of diagnostics services – Agilus Diagnostics Ltd with over 400 labs and 4,100+ customer touchpoints and a growing presence across 1,000+ towns and cities. In addition to India, the company also has presence in UAE, Nepal and Sri Lanka.

Products and Services

The company’s services can be categorised into two segments:

- Healthcare includes inpatient and outpatient services, sale of medical and non-medical items and management fees from hospital.

- Diagnostics include pathology and radiology services.

Subsidiaries: As of FY25, the company has 29 subsidiaries and 2 associates and joint ventures each.

Investment Rationale

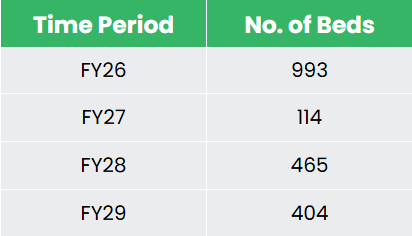

- Expansion plans – Fortis has set out aggressive expansion strategy, aiming to add approximately 2,000 beds between FY26 and FY29 through a combination of acquisitions, brownfield developments, and greenfield projects. The company has acquired entire operations (underlying hospital and adjacent land) of Shrimann Superspecialty Hospital, Jalandhar, one of the leading multi-specialty hospitals in the region, which reported revenue of Rs.138 crore in FY24. This acquisition has added 228 beds to the company’s portfolio, with potential to further expand capacity by over 180 beds through the development of a new facility on the adjacent land. During FY25, Fortis commissioned its newly built 350-bed hospital in Manesar, starting operations with an initial capacity of 90 beds. The facility, currently operating at 40% occupancy, has achieved an ARPOB of Rs.2.67 crore. The company plans to add another 120 beds and targets an occupancy rate of 50% by FY26. Within its diagnostics arm, it is upgrading its infrastructure through the commissioning of advanced medical equipment. A new genomics lab has been launched in Gurgaon, alongside a transplant immunology lab in Bangalore, further strengthening its capabilities in specialized diagnostics The below table gives additional capacity expansion plans currently announced by the company:

- Operational Performance – The company delivered strong operational performance in FY25, underpinned by improved hospital metrics, rising procedural volumes, and growth across key specialties and geographies. Overall hospital occupancy improved to 69% from 65% YoY, reflecting higher patient volumes and improved capacity utilization. The Average Revenue Per Occupied Bed (ARPOB) increased to Rs.2.42 crore p.a. from Rs.2.22 crore p.a., driven by higher case complexity and increased contribution from high-yield specialties. Key clinical segments – including oncology, neurosciences, cardiac sciences, gastroenterology, orthopaedics, and renal sciences – grew by 16% YoY, collectively contributing 62% to the total hospital revenue. The Average Length of Stay (ALOS) improved from 4.28 days to 4.19 days, indicating operational efficiency and better case management. Revenue from digital channels registered a robust growth of 35% and international patient revenues rose 13% YoY to Rs.539 crore. In terms of procedural volumes, the company reported a significant 72% YoY growth in robotic surgeries and a 17% increase in neuro and spine procedures, highlighting rising demand for advanced surgical care.

- Q4FY25 – During the quarter, the company generated revenue of Rs.2,007 crore, achieving an increase of 12% as compared to the Rs.1,786 crore of Q4FY24. EBITDA improved by 14% YoY, from Rs.435 crore to Rs.380 crore. Net profit stood at Rs.188 crore, a de-growth of 7% from Rs.203 crore of Q4FY24.

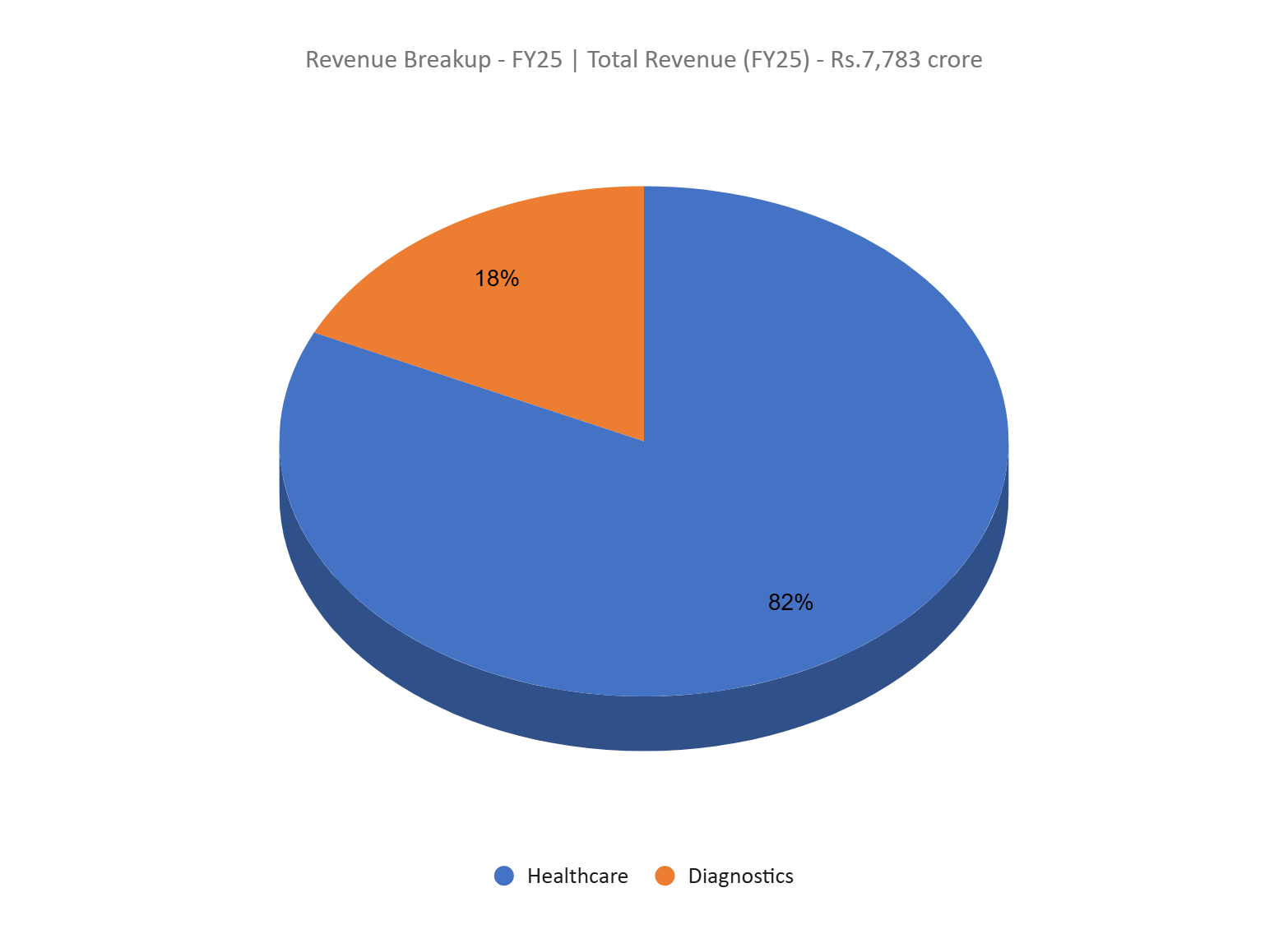

- FY25 – The company generated revenue of Rs.7,783 crore, an increase of 13% compared to FY24 revenue. The growth was primarily driven by ~15% growth in hospital business revenue which contributes 84% to the company’s revenue. EBITDA is at Rs.1,655 crore, up by 27% YoY. The company posted a net profit of Rs.809 crore, a growth of 25% YoY. EBITDA margin has improved from 19% to 21% and net profit margin improved from 9% to 10%. Hospital business has improved its EBITDA margin from 19% to 21% and diagnostics arm EBITDA margin from 17% to 20%.

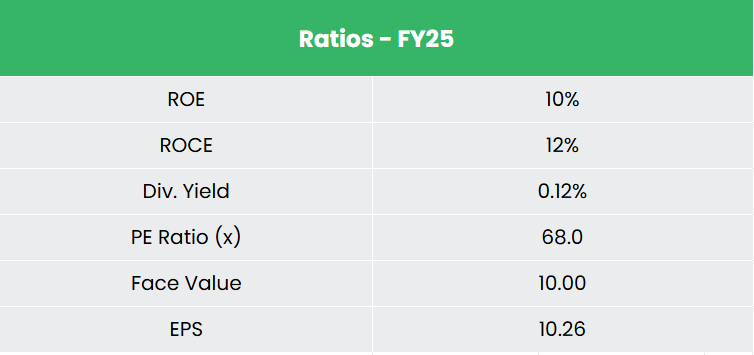

- Financial Performance – The revenue and net profit CAGR of the company for the past 3 years is around 11% and 31% between FY23-FY25. The 3-year average ROE and ROCE for the company is around 9% and 11% for the past 3 years. The company has a healthy capital structure with a debt-to-equity ratio of 0.28.

Industry

India’s healthcare sector has emerged as one of the country’s largest industries, both in terms of revenue generation and employment. In 2023, the hospital market was valued at US$ 98.98 billion and is expected to grow at a compound annual growth rate (CAGR) of 8.0% from 2024 to 2032, reaching approximately US$ 193.59 billion by 2032. The country has also positioned itself as a leading hub for advanced diagnostic services, supported by significant capital investments. India is also a cost-effective option compared to other countries in Asia and the West, making it an attractive destination for international patients and contributing to the rise of medical tourism.

Growth Drivers

- Government allocation of Rs.99,858 crore (US$ 11.50 billion) to the healthcare sector in the Union Budget 2025-26, a 9.78% increase compared to the previous year.

- 100% FDI allowed under automatic route in the hospital sector.

- Rising income levels, ageing population, growing health awareness and greater penetration of health insurance.

Peer Analysis

Competitors: Aster DM Healthcare Ltd, Global Health Ltd etc.

We believe the company is fairly valued relative to its peers, supported by strong fundamentals, robust revenue growth, consistent returns on invested capital, and stable operating margins that reflect disciplined cost management and operational efficiency.

Outlook

For FY26, the company has provided revenue growth guidance of 14–15%, with 5–6% expected to come from higher ARPOB, and the remainder driven by increased patient volumes. The hospital business is expected to achieve an EBITDA margin of 20.5%, while the diagnostics segment is guided to deliver margins in the range of 21% to 22%. Over the medium term, the company is targeting EBITDA margins of 25%. On the expansion front, Fortis continues to scale through brownfield projects. In Punjab, the company plans to double its current bed capacity from approximately 800 to 1,600 beds in the next 2–3 years, supported by ongoing and planned brownfield developments in key cities such as Amritsar and Mohali.

Valuation

We believe the company is well positioned to capitalise on the rising healthcare demand, supported by consistent bed additions and operational efficiencies. We recommend a BUY rating in the stock with the target price (TP) of Rs.948, 64x FY27E EPS.

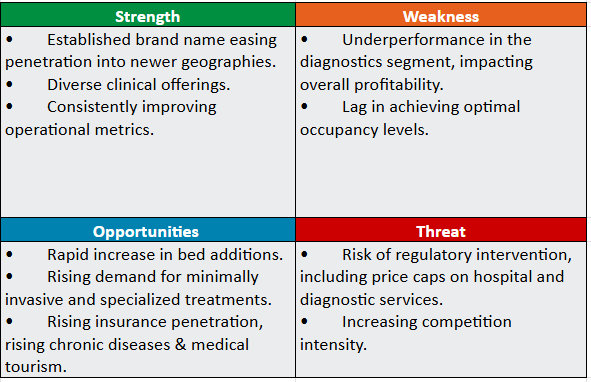

SWOT Analysis

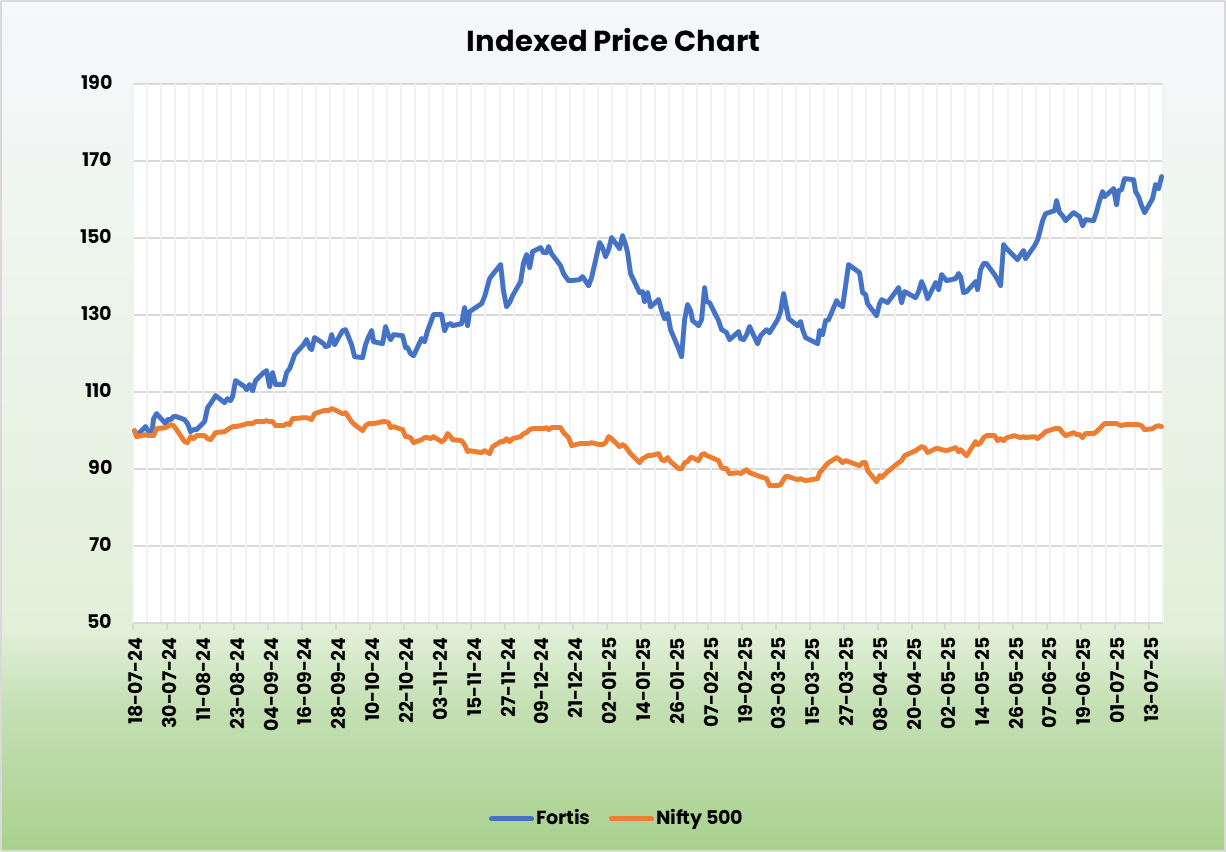

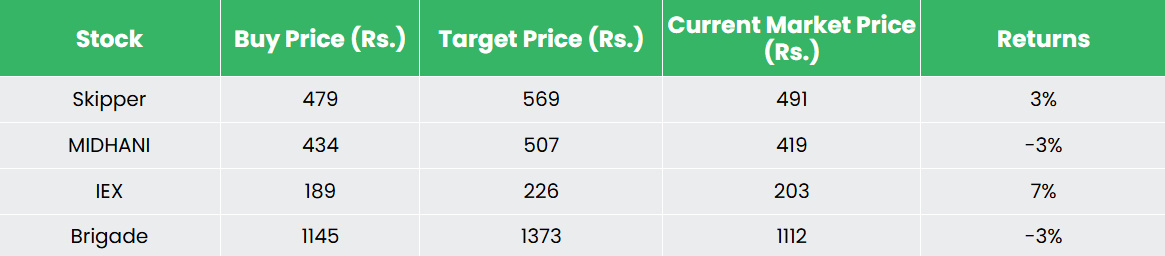

Recap of our previous recommendations (As on 18 July 2025)

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.

Other articles you may like

Post Views:

249