Rising costs, low financial awareness impact

As the cost of living continues to rise, young Australians are increasingly turning to loans to manage their finances, according to Lendela.

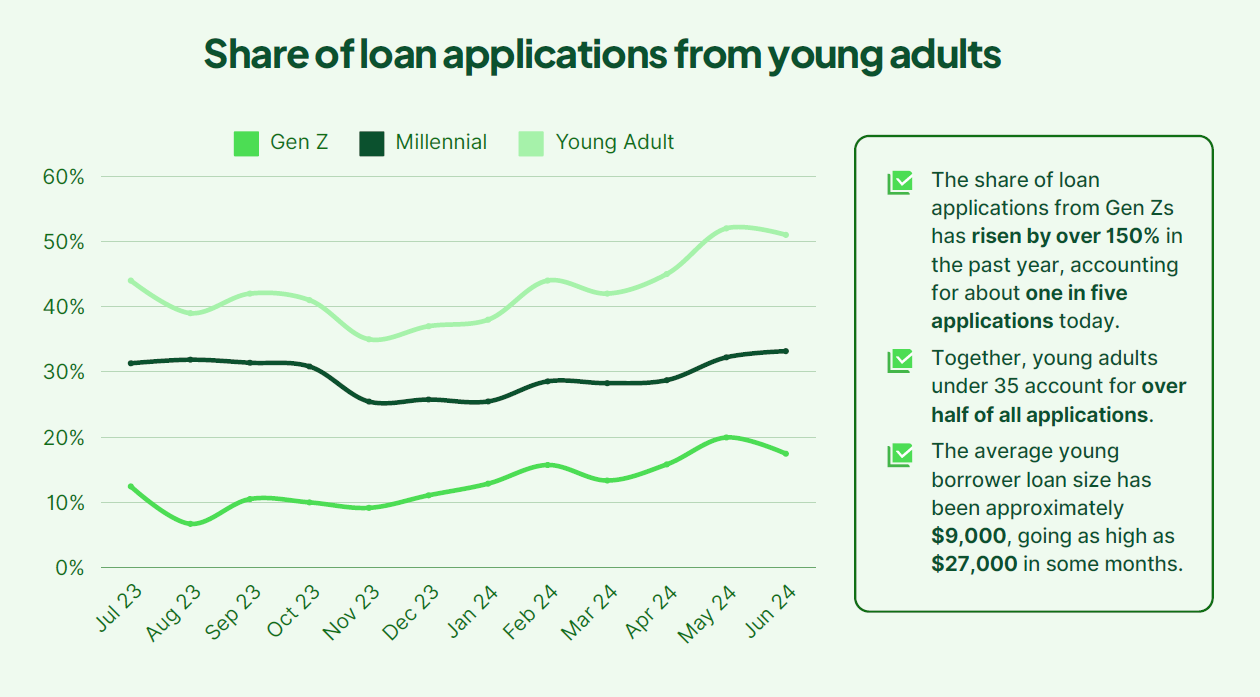

“Over the past year, we’ve seen a rapid spike in the share of loan applications coming from Gen Zs and Millennials, largely to cope with rising costs,” said Jake Osborne (pictured above), Australia country manager at Lendela.

Lack of credit awareness hurts borrowers

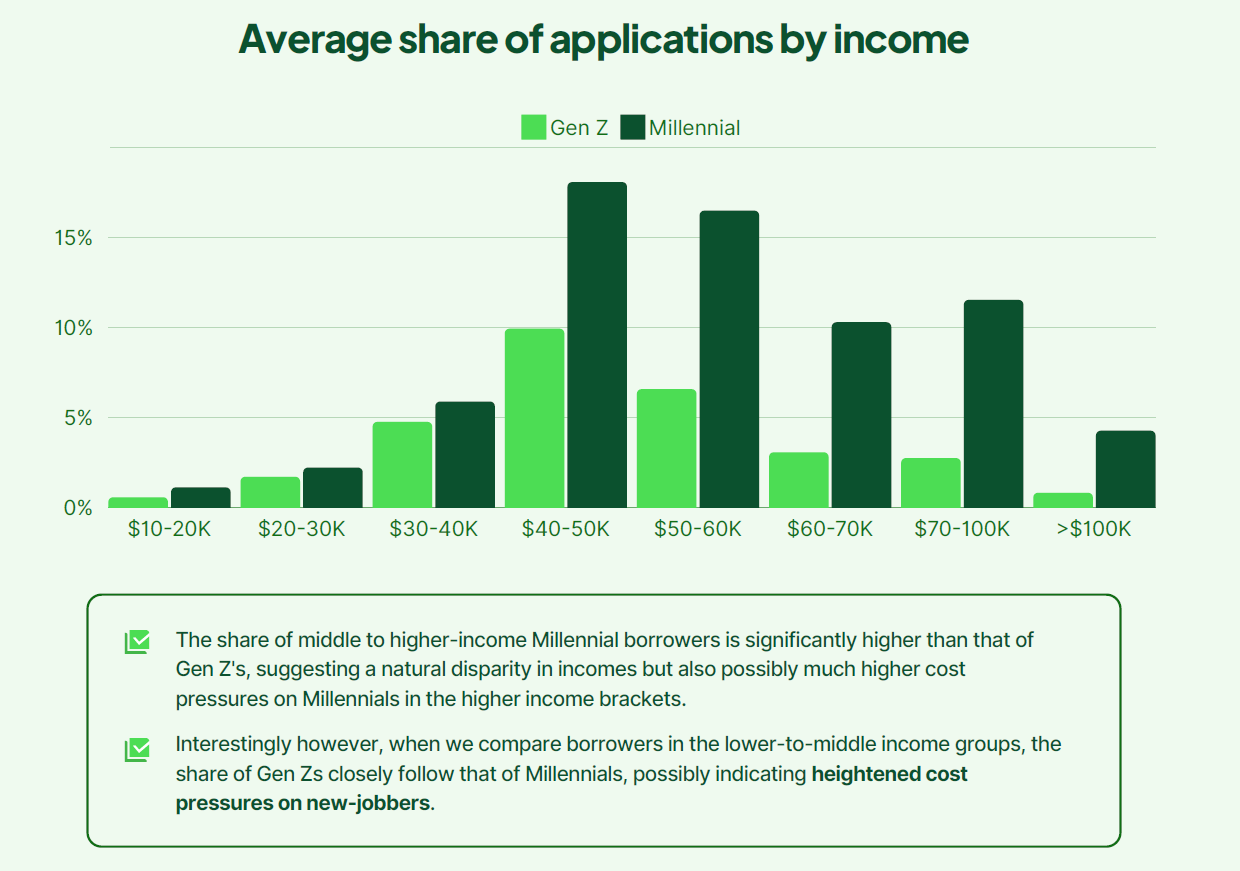

Lendela’s study revealed a concerning trend: many young borrowers lack awareness of credit management, leading to lower credit ratings and higher existing debts.

“On closer look, however, we see signs that point to a lack of awareness of credit management among younger borrowers,” Osborne said.

Importance of responsible borrowing

Osborne stressed the need for responsible borrowing, especially during economic hardship.

“It’s important to recognize that our credit profiles, including payment conduct, will dictate what options we have available to us and at what costs,” he said.

Debt consolidation as a solution

One way young Australians are managing their debts is through debt consolidation, which allows them to service a single loan with a more manageable interest rate.

Osborne shared that many borrowers have explored this option to reduce costs.

“Borrowers with multiple debts have explored this route to bring costs down,” he said.

Loan matching key to competitive offers

Osborne advised that young Australians should explore all available options before committing to a loan.

“Simply comparing and applying across multiple lenders at the same time will hurt their credit scores,” he said.

He highlighted the importance of loan matching to find the most competitive offers in today’s climate.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.

Related Stories

Keep up with the latest news and events

Join our mailing list, it’s free!