{kind=link}

Indian Hotels Co Ltd – Leading with Luxury and Scale

Incorporated in 1902 and headquartered in Mumbai, The Indian Hotels Company Ltd. (IHCL) is primarily engaged in the business of owning, operating & managing hotels, palaces, and resorts. A part of Taj Group, the company operates its hotels under 4 main brands catering to different segments viz. luxury Taj, upscale/ upper upscale Vivanta/ SeleQtions and midscale/ lean luxury Ginger segments. Additionally, IHCL’s portfolio includes diverse F & B, wellness, salon, and lifestyle brands through its brands amã Stays & Trails – experimental homestay segment, Taj SATS Air Catering – 46+ years of catering experience in flights, Qmin – food delivery service app from IHCL’s signature restaurants. As of 30 June 2025, the company has portfolio of 392 hotels (249 operational and 143 in pipeline).

Products and Services

IHCL builds and manages hotels under various formats – luxury, upscale, select and lean luxe hotels. It offers a wide spectrum of other services such as air catering, salons and spas, food and beverages, boutiques, stays and trails and business clubs.

Subsidiaries: As of FY25, the company has 33 subsidiaries, 6 associates and 6 joint venture companies.

Investment Rationale

- Growth Strategies – The company continues to deliver robust growth through its capital-light strategy, focusing on managing and operating hotels rather than owning them outright. In FY25, the company signed 74 hotels and opened 26, with over 95% of signings being asset-light, supporting improved ROCE. Management fees rose 20% to Rs.562 crore in FY25, while capital-light growth also led to a 17% YoY increase in management fees to Rs.133 crore in Q1FY26. The company is also capitalizing on India’s fast-growing mid-scale and upscale segments through Ginger, Vivanta and Gateway, with Ginger crossing the 100-hotel mark and Vivanta surpassing 50. Additionally, the Qmin integration within Ginger now contributes 95% of its new business revenue. Strengthening customer engagement, the Tata Neu loyalty program crossed 10 million members, with direct bookings growing 43% YoY to over Rs.2,200 crore, further enhancing profitability through improved channel mix.

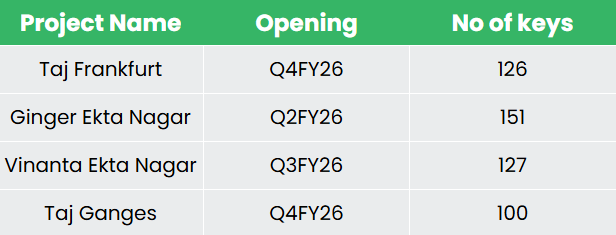

- Expansion plans – Under its ambitious “Accelerate 2030” strategy, the aims to double its revenue, achieve ROCE of over 20%, and expand its portfolio to over 700 hotels. In Q1FY26, the company signed 12 new hotels and opened 6 properties, including international portfolio. Looking ahead, IHCL plans to open 30+ hotels in FY26. Key projects in the pipeline for the year include:

- Operational Performance and RevPAR Leadership – The company delivered strong operational performance, underpinned by robust growth in Revenue Per Available Room (RevPAR) and increased digital bookings. The company reported a 13% YoY increase in consolidated RevPAR, rising from Rs.11,500 in Q1FY25 to Rs.13,000 in Q1FY26. Consolidated room revenue also rose by 13% to Rs.877 crore. A key highlight was the rising share of direct bookings through IHCL’s own website, contributing to improved cost efficiencies. Notably, IHCL maintained a RevPAR premium of 73% over the industry average at the enterprise level, reinforcing its leadership and premium positioning across all market segments.

- Q1FY26 – During the quarter IHCL generated revenue of Rs.2,041 crore, an increase of 32% YoY compared to the Rs.1,550 crore of Q1FY25. Profits improved, with operating profit increasing by 28% YoY to Rs.637 crore (vs Rs.496 crore of Q1FY25) and net profit surging by 36% YoY to Rs.319 crore (vs Rs.234 crore of Q1FY25).

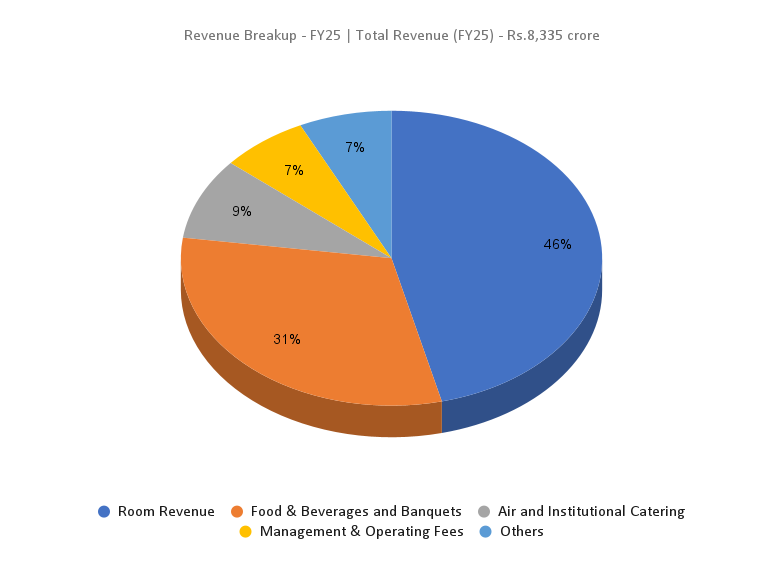

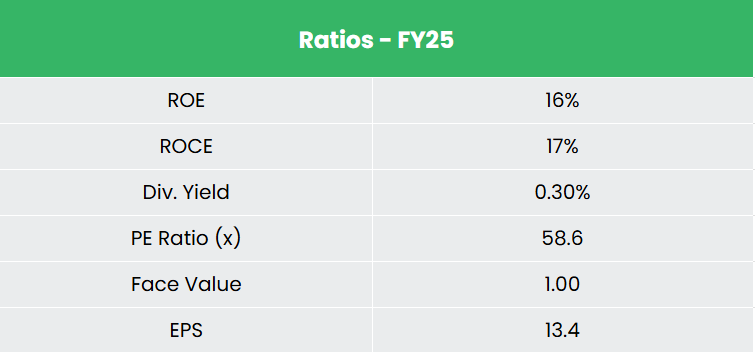

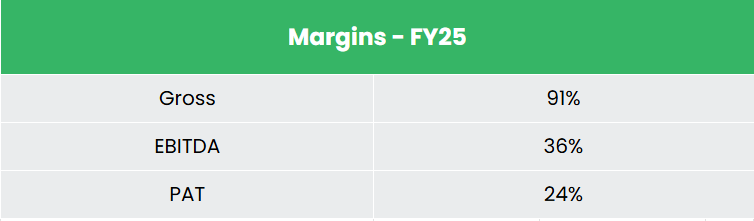

- FY25 – During the financial year, the company generated revenue of Rs.8,335 crore, an increase of 23% compared to FY24 revenue. Operating profit is at Rs.3,000 crore, up by 28% YoY. The company posted a net profit of Rs.1,961 crore, an increase of 63% YoY. Operating profit margin improved from 35% to 36% and net profit margin increased from 18% to 24%.

- Financial Performance – IHCL has generated revenue and PAT CAGR of 40% and 97% over the period of 3 years (FY23-25). The average 3-year ROE & ROCE is around 15% each for the FY23-25 period. The company has a strong balance sheet with a robust debt-to-equity ratio of 0.28. The company is holding a robust cash reserve of ~Rs.3,000 crore.

Industry

India’s tourism and hospitality industry is a key driver of economic growth, supported by its rich cultural diversity, increasing domestic demand, and strong government initiatives. Contributing approximately US$ 199.6 billion to GDP, the sector is projected to reach US$ 512 billion by 2028. Government programs like Swadesh Darshan 2.0, Heal in India, and expanded e-Visa schemes are enhancing infrastructure and attracting both international and domestic tourists. Trends such as staycations and rising medical and spiritual tourism are further boosting demand. As one of the fastest-growing service sectors, it plays a vital role in job creation, foreign exchange earnings, and sustainable development.

Growth Drivers

- Allocation of Rs. Rs. 2,541.06 crore in the Union Budget 2025-26 towards the tourism sector.

- 100% Foreign Direct Investment (FDI) allowed in the tourism and hospitality under automatic route.

- Government initiatives, such as the @2047 Vision, aiming to attract 100 million inbound tourists by 2047.

Peer Analysis

Competitors: Lemon Tree Hotels Ltd, ITC Hotels Ltd, etc.

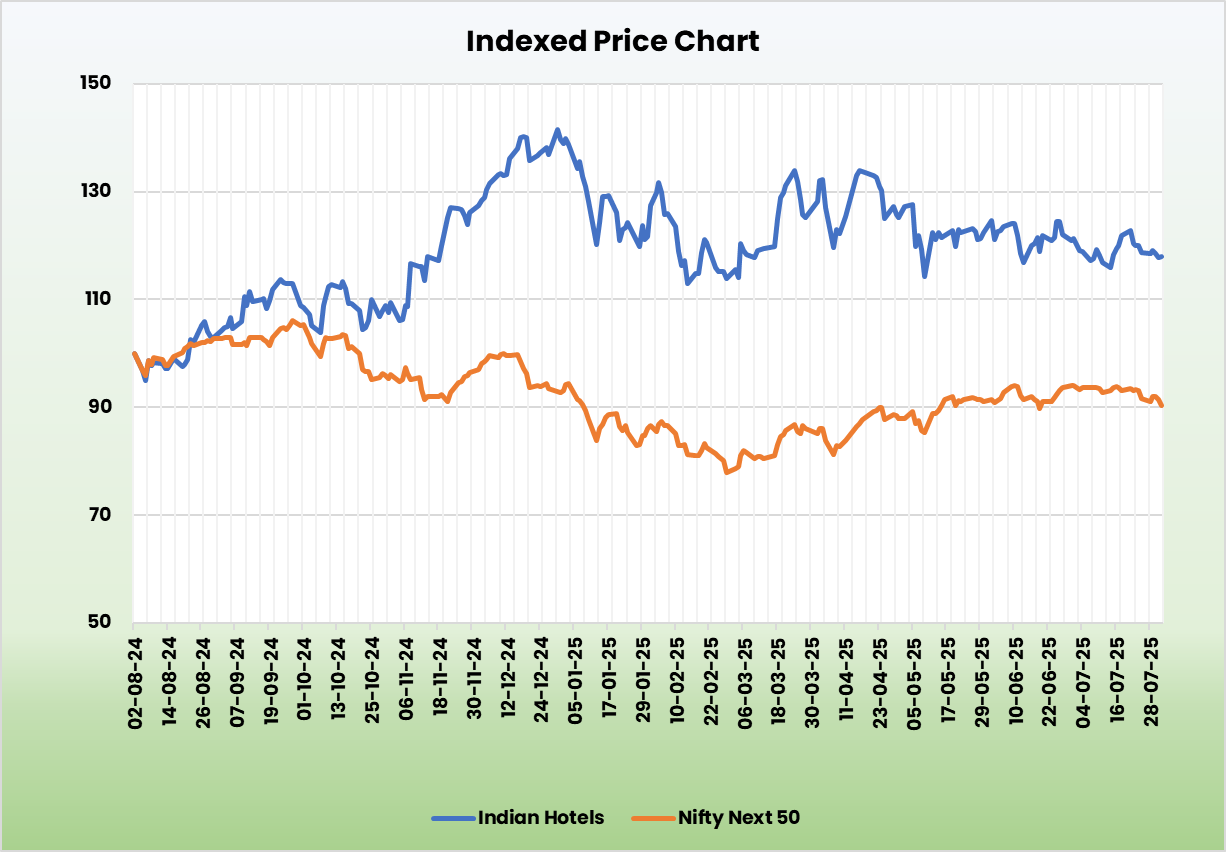

Compared to the above competitors, IHCL is the most undervalued stock with robust returns on the capital invested and healthy growth in sales.

Outlook

The company is projecting double-digit revenue growth in FY26 and has earmarked a capex of Rs.1,200 crore, marking a 20% increase over FY25. This investment will support ongoing asset construction, property renovations, capacity expansion, and digital transformation initiatives. IHCL’s new business verticals—including Ginger, Qmin, Ama Stays & Trails, and Tree of Life—posted a robust 40% revenue growth in FY25. These ventures remain margin accretive, delivering a consolidated margin of 37%, compared to the company-wide margin of 35%. Additionally, IHCL is witnessing strong recovery in key international markets such as the US and UK and is expanding its global footprint with new projects in South Africa and Germany, aligning with its strategy to deepen international presence.

Valuation

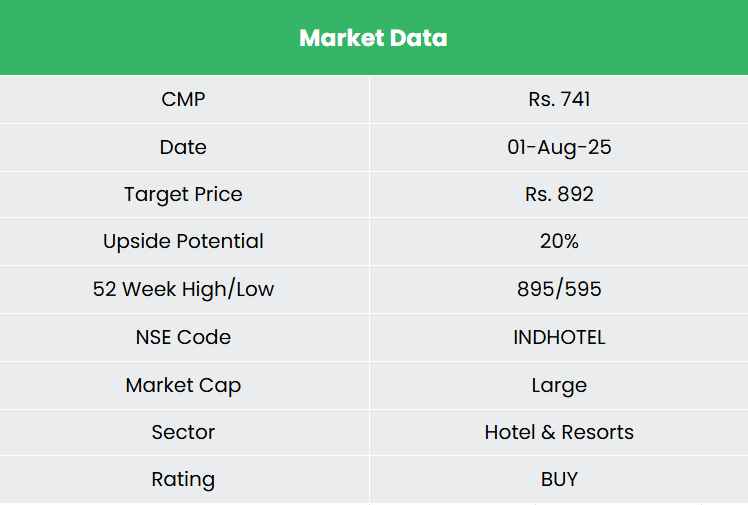

We believe the company offers a compelling investment opportunity driven by its strong brand equity, consistent operational performance, and strategic expansion in high-growth domestic and international markets. We recommend a BUY rating in the stock with the target price (TP) of Rs.892, 53x FY27E EPS.

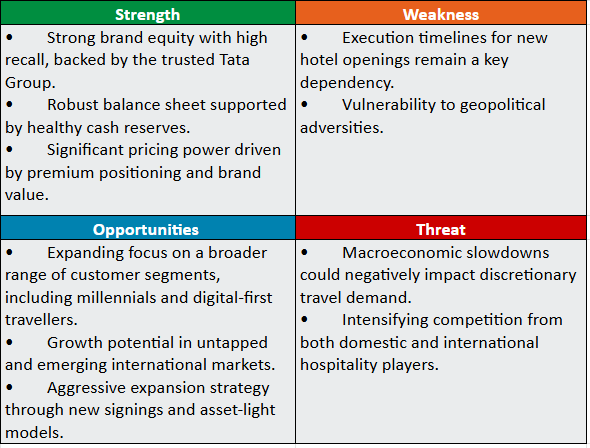

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.

Other articles you may like

Post Views:

210