{kind=link}

Narayana Hrudayalaya Ltd – Health for all. All for health.

Narayana Hrudayalaya Limited, incorporated in 2000 and headquartered in Bengaluru, is one of India’s leading multi-specialty healthcare providers, operating an integrated network of 42 healthcare facilities comprising 18 hospitals, 2 heart centres, and 20 clinics and dialysis centres in India, along with 2 hospitals in the Cayman Islands, aggregating to 5,554 operational beds as of H1FY26. The group focuses on tertiary and quaternary care, with strong presence across cardiac sciences, oncology, neurosciences, orthopaedics, nephrology, gastroenterology, and organ transplantation, and is among the highest-volume providers of complex cardiac and transplant procedures in the country. During FY25, Narayana Health delivered care to over 247,000 outpatients and 30,000 inpatients, performing ~8,500 surgeries, supported by a workforce of over 14,900 employees, and maintained an average length of stay of 3.79 days. Its hospital network is anchored by flagship centres such as Narayana Health City, Bengaluru, and Health City Cayman Islands, and is supported by in-house digital platforms including ATHMA (EMR) and Medha (AI).

Products and Services

- Healthcare: Cardiac, oncology, neurosciences, organ transplantation, orthopaedics, gastrointestinal care.

- Ancillary Services: Hospital operations, diagnostics, preventive care, pharmaceuticals, overseas tertiary care.

- Digital & Technology: ATHMA, Medha, NH Care App, YASA platform.

- Insurance: Health insurance through integrated care ecosystem and subsidiaries.

Subsidiaries: As of FY25, the company has 15 subsidiaries and 1 associate company.

Investment Rationale

- Shift from Capacity-Led Growth to Monetisation and Efficiency – Management’s strategy is clearly pivoting from aggressive bed expansion to improving monetisation and efficiency of existing assets. Despite largely stable operational bed capacity, Narayana Health delivered a ~14% YoY increase in ARPOB to Rs.17.5 mn in Q2FY26, indicating higher revenue extraction per bed. Revenue growth is increasingly driven by payer mix optimisation, with insured and corporate patients contributing a higher share, alongside a greater focus on high-acuity, complex specialties such as cardiac, oncology and neurosciences. Margin expansion to ~24% EBITDA further underscores the benefits of cost optimisation and operating leverage. Capex remains targeted towards technology, robotics and quaternary care capabilities rather than new hospitals, reinforcing a “sweat-the-assets” strategy. This shift enhances ROCE, improves earnings visibility and reduces execution risk versus capacity-led growth.

- UK Acquisition: Cayman Playbook Scaled with Limited Balance Sheet Risk – Narayana Health’s acquisition of 100% of Practice Plus Group Hospitals marks its entry into the UK through a scaled secondary-care platform with strong revenue visibility. The transaction is debt-free at the operating level, with NH assuming only operating liabilities while all term debt remains with the seller, limiting balance sheet risk. The asset comprises ~330 operational beds focused on elective procedures such as orthopaedics, ophthalmology and general surgery, with ~90%+ revenues derived from long-term NHS contracts and headroom to increase private/self-pay mix over time. Management intends to replicate the Cayman playbook by deploying NH’s technology and operating discipline to improve throughput and margins, targeting ~20–22% ROCE by FY29 – 30.

- Insurance Integration: Embedded Volume and ROCE Upside – NH’s entry into health insurance through a wholly owned subsidiary is a rare strategic differentiator among listed hospital peers, most of whom have exited or avoided insurance ownership. While standalone insurance profitability will take time given initial losses and regulatory capital requirements, the near-term value lies in indirect synergies. Integrated insurance can improve patient affordability, reduce claim friction, and drive higher customer stickiness and utilisation across NH’s hospital and clinic network. Early traction is visible, with Cayman insurance revenues scaling from ~US$0.6 mn in Q2FY25 to ~US$9.3 mn by Q2FY26 on strong employer adoption. In India, the pilot has covered ~4,000 lives across Bangalore and Mysore, with recent expansion to Kolkata, underscoring improving acceptance and execution momentum. Vertical integration enables NH to capture a larger share of patient lifetime value and smoothen revenue visibility. Over time, access to claims and treatment data can support better cost control and underwriting discipline. If executed well, insurance can structurally lift volumes, ROCE and competitive positioning, creating a non-linear growth lever beyond core hospital expansion.

- Q2FY26 – During the quarter, the company reported consolidated operating revenue of Rs.1,644 crore, up 20% YoY compared to Rs.1,367 crore in Q2FY25. EBITDA rose to Rs.431 crore, a 30% YoY increase from Rs.332 crore, with EBITDA margin expanding from 24.3% to 26.2%, reflecting operating leverage and improved profitability. Net profit stood at Rs.258 crore, up 30% YoY from Rs.199 crore, supported by higher surgical volumes, including a record number of robotic and minimally invasive cardiac procedures at Narayana Institute of Cardiac Sciences, Bengaluru, and the commissioning of Bone Marrow Transplant (BMT) services at the Jaipur facility, expanding the group’s quaternary care capabilities during the quarter.

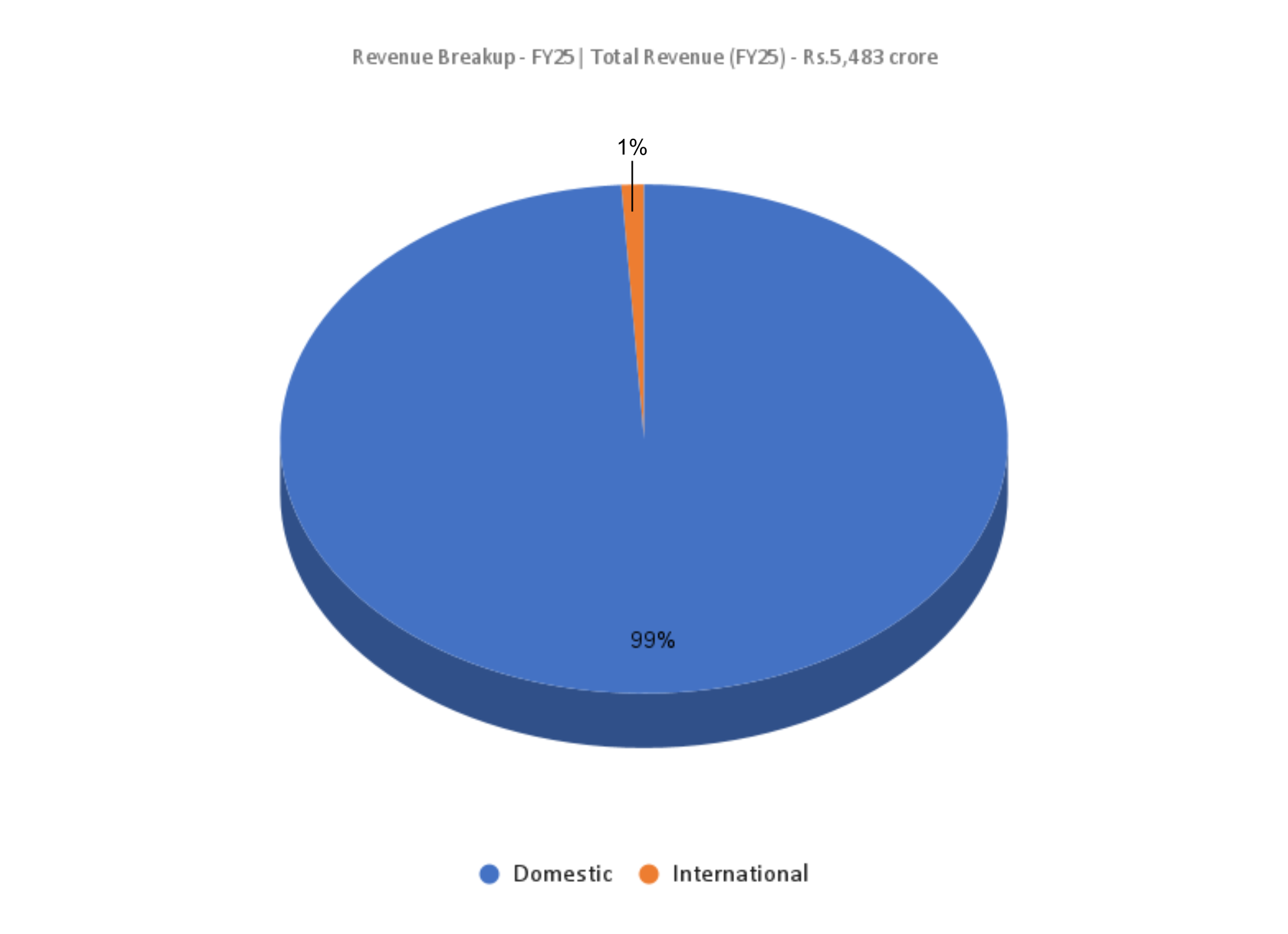

- FY25 – During FY25, the company reported consolidated operating revenue of Rs.5,483 crore, representing a 12% YoY increase compared to Rs.4,890 crore in FY24. EBITDA stood at Rs.1,368 crore, up 12% YoY, and net profit was recorded at Rs.790 crore, broadly flat with Rs.786 crore in FY24, as higher finance costs and a normalized effective tax rate offset operating growth.

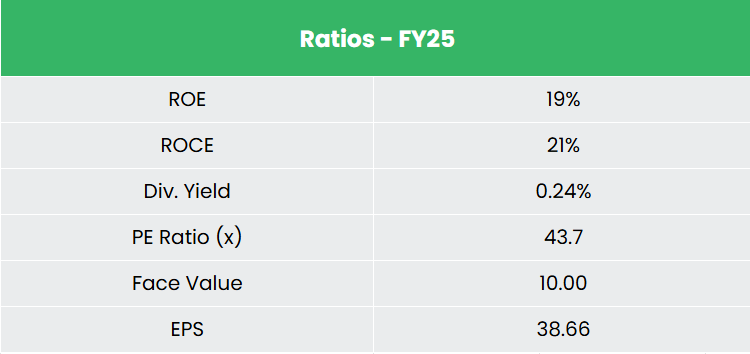

- Financial Performance – The 3-year revenue and net profit CAGR stands at 14% and 31% respectively between FY23-25. The company has a debt-to-equity ratio of 0.58. The 3-year average ROE and ROCE are around 29% and 26% for FY23-25 period.

Industry

The Indian healthcare sector is among the fastest-growing segments of the domestic economy, supported by favourable demographics, rising income levels, and improving access to medical services. The sector has seen unprecedented growth in the recent years, driven by expansion across hospitals, pharmaceuticals, diagnostics, and digital health. Within this, the hospital segment remains the largest and most capital-intensive vertical. Healthcare spending in India continues to trend upward, with total expenditure expected to rise from 3.3% of GDP in 2022 to ~5% by 2030, while public sector support remains meaningful, reflected in a Rs.99,858 crore allocation in the Union Budget FY26. The combination of structural demand growth, capacity constraints, and policy support continues to provide long-term visibility for organised hospital operators.

Growth Drivers

- India’s hospital bed density remains well below global benchmarks and policy targets, creating a structural supply gap. Coupled with rising utilisation of organised healthcare, this underpins sustained demand for private hospital capacity expansion.

- Government initiatives such as Ayushman Bharat and PM-ABHIM, along with a Rs.99,858 crore allocation in the Union Budget FY26, continue to improve healthcare affordability and utilisation across public and private systems.

- The sector benefits from liberal investment norms, with 100% FDI permitted under the automatic route for greenfield projects, and cumulative FDI inflows $ 12.25 billion into hospitals and diagnostics between April 2000 and June 2025.

Peer Analysis

Competitors: Global Health Ltd and Max Healthcare Institute Ltd, etc.

Compared to its peers, the company demonstrates disciplined capital allocation and strong profitability and financial performance.

Outlook

The outlook remains favourable, supported by sustained demand for organised healthcare, improving payer mix and operating leverage from existing assets. Management’s focus on monetisation, cost efficiency and ecosystem-led growth (insurance and clinics) should support margin expansion and ROCE improvement. International operations, led by Cayman and the UK, add incremental growth optionality with limited balance sheet risk.

Valuations

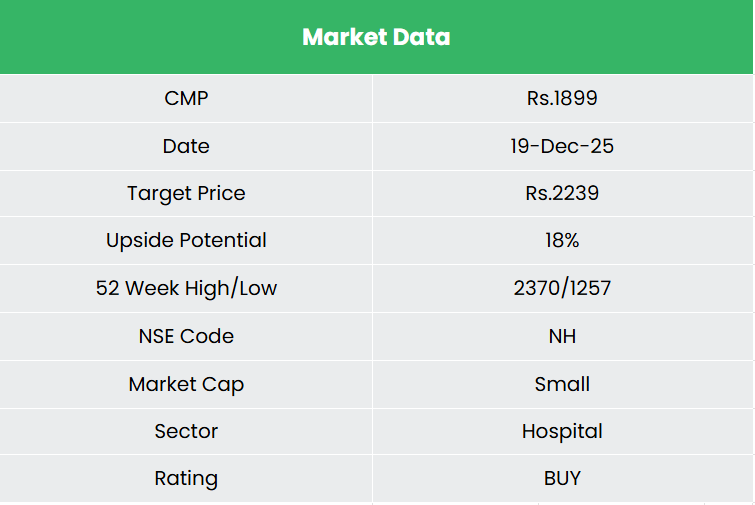

Given its focus on improving patient stickiness through long-term care facilities and insurance offerings, along with forward-looking AI and digital capabilities, we believe the company presents a strong long-term investment opportunity. We recommend a BUY rating in the stock with the target price (TP) of Rs.2,239, 44x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

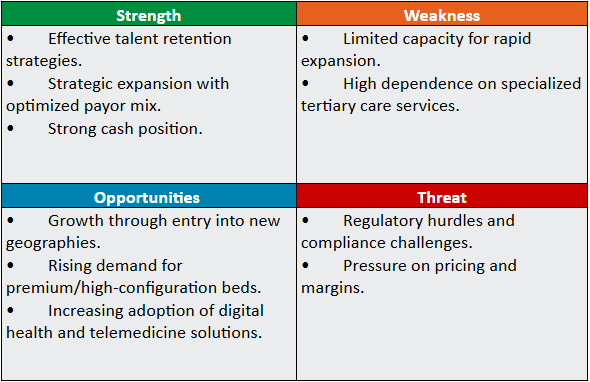

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.

Other articles you may like

Post Views:

29